in this case

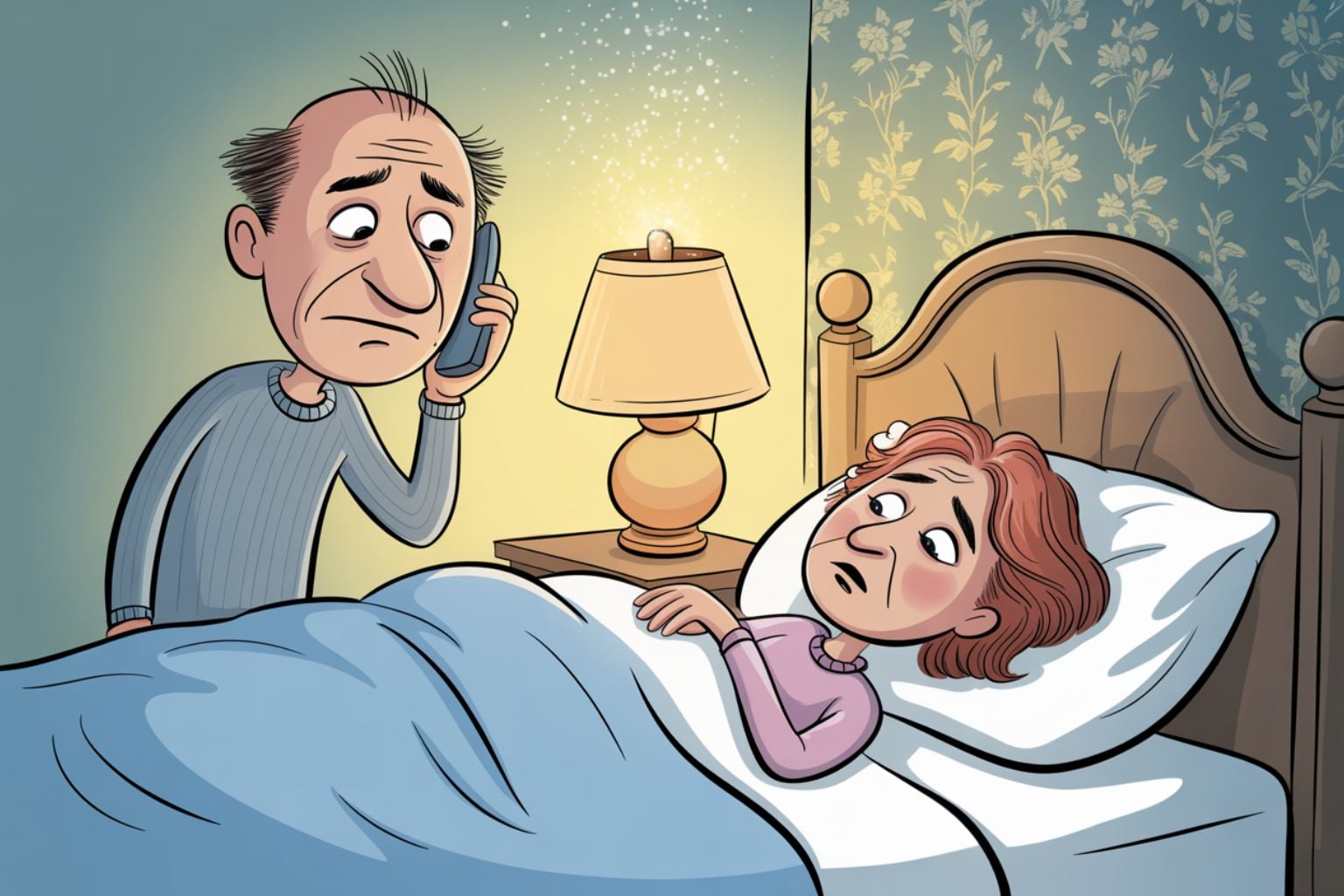

- Bill Chellis’s wife woke up with a 102-degree fever and severe cough on the morning of their Hampton Inn stay. She was later diagnosed with pneumonia and hospitalized.

- He called to cancel but was told he’d still be charged the full $173 for late cancellation. The hotel manager never returned his calls.

- Chellis called Hilton customer service, wrote to corporate offices, and sent a certified letter. No one responded to any of his requests for a refund or credit.

When Bill Chellis’s wife falls seriously ill on the morning of a hotel stay, he does what most of us would do. He calls the Hampton Inn in Great Falls, Mont., to cancel. But instead of compassion, he gets a bill for the full stay.

Question

My wife and I were booked into the Hampton Inn in Great Falls, Mont. On the morning of our trip, she woke up with a 102-degree fever and a severe cough. She was later diagnosed with pneumonia and had to be admitted to the hospital.

I called the hotel to cancel the reservation, but the desk clerk told me we’d still be charged the full $173 because it was a late cancellation. He said there was nothing he could do.

I called Hilton’s customer service line, and a representative said the property would have to handle it. I asked for the hotel manager, but she was in a meeting. I left my number but never heard back.

I later wrote to Hilton’s corporate offices and even sent a certified letter to Hilton corporate, but no one responded. I just want a refund or a credit for a future stay.

Can you help me? —Bill Chellis, Camano Island, Wash.

Answer

I’m sorry to hear about your wife’s illness and I hope she’s feeling better. Hotels typically have strict cancellation policies. Most major chains require 24 hours’ notice or more to avoid penalties. In your case, Hilton was within its rights to charge for the night. But in the hospitality business, having the right to do something and doing the right thing are often not the same.

Your paper trail shows you did everything you could to get help. You called, you asked for a manager, you appealed to corporate, and you followed up in writing. (By the way, you can find the names, numbers and email addresses of the Hilton executives on my consumer advocacy site, Elliott.org,) That’s exactly what consumers should do when they have a legitimate request for an exception to policy.

Washington State has a Consumer Protection Act that broadly prohibits “unfair or deceptive” practices. While it doesn’t specifically cover hotel cancellations, it does give consumers a legal avenue if a company refuses to act in good faith. On a federal level, there’s no blanket law requiring hotels to waive penalties for medical emergencies, but the Federal Trade Commission does monitor businesses for misleading practices. The “may incur charges” wording in Hilton’s own cancellation notice arguably left the door open for some discretion.

When I contacted Hilton, it reviewed your case again. A representative said its front desk agent had correctly followed policy but confirmed that it overlooked your follow-up requests. Hilton refunded your $173.

Your case is a good reminder that policies are not always the final word. If you have a valid reason, backed up by documentation, and you politely persist, companies can often bend a rule. And when they don’t? Well, you know how to find me.

I hope the letter writer’s wife is well, and I’m sorry to hear about her illness, but her illness wasn’t Hilton’s fault. Of course they bent the rule and refunded the money once Chris got involved, for PR reasons, but this a case Chris shouldn’t have taken. If we expect companies to follow the rules when it comes to how they treat us, and we should expect that, it’s on us to respect the rules as well.

Read more insightful reader feedback. See all comments.

Your voice matters

Your wife is hospitalized with pneumonia. You call to cancel. The hotel charges you anyway and ignores your calls, letters, and certified mail for months.

- Should hotels be legally required to waive cancellation fees when guests provide medical documentation of hospitalization on the day of check-in?

- Should hotel chains be required to respond to customer service complaints within 14 days or face automatic refunds for disputed charges?

- Should hotels be prohibited from charging cancellation fees when the guest never occupied the room and the hotel has the opportunity to resell it?

How do hotel cancellation rules work when you have a medical emergency?

Quick answers to the most common questions travelers have about canceling a hotel reservation due to illness, based on this Hampton Inn case and Elliott Advocacy’s consumer guidance.

Yes. Most hotels, including Hilton-brand properties like Hampton Inn, can legally charge the full nightly rate if you cancel inside the cancellation window, typically 24 to 48 hours before check-in. There is no federal law requiring hotels to waive cancellation fees for illness, but many chains will refund the charge as a goodwill gesture if you provide documentation and escalate politely.

Hampton Inn’s standard flexible rate generally requires cancellation by 11:59 p.m. local time the day before arrival to avoid a one-night charge. Advance-purchase and prepaid rates are usually nonrefundable. Hilton’s booking terms state guests “may incur charges” for late cancellations, which leaves room for the hotel to use discretion in cases like medical emergencies. See Elliott Advocacy’s ongoing Hilton coverage for recent cases.

Start by calling the property directly and politely asking the front desk or general manager for an exception. If that fails, escalate in writing to the brand’s corporate customer service, then to an executive contact. Include a clear paper trail: booking confirmation, dates, names of everyone you spoke with, and documentation of the emergency, such as a doctor’s note or hospital discharge paperwork. Elliott Advocacy’s guide to how consumer complaints work walks through the full escalation path.

Elliott Advocacy publishes a directory of Hilton executive names, phone numbers, and email addresses on the Hilton company contacts page. Use these contacts only after the front desk, customer service line, and standard corporate channels have failed to resolve your issue.

Most comprehensive travel insurance policies reimburse prepaid, nonrefundable hotel costs if you cancel because of a covered medical reason, such as a sudden illness or hospitalization. You will usually need a physician’s statement confirming you were unfit to travel. “Cancel for Any Reason” (CFAR) add-ons provide broader coverage but typically refund only 50 to 75 percent of your trip cost. For more detail, see Elliott Advocacy’s guide to buying travel insurance.

At the state level, laws like the Washington Consumer Protection Act (RCW 19.86) prohibit “unfair or deceptive” business practices and give consumers a path to file a complaint or small-claims action. Federally, the Federal Trade Commission monitors misleading business practices but does not regulate hotel cancellation fees directly. You can also file a complaint with your state attorney general.

You can file a credit card chargeback, but it should be a last resort after you have exhausted direct negotiation with the hotel. Chargebacks for “services not rendered” rarely succeed when the hotel followed its published cancellation policy. A stronger case is possible if the hotel promised a refund in writing and then failed to process it. Elliott Advocacy’s complete guide to chargebacks covers the process in detail.

Can a hotel charge you if you cancel because of a medical emergency?

What is Hilton’s cancellation policy for Hampton Inn reservations?

How do I get a refund from a hotel after a late cancellation?

Where can I find Hilton executive contacts to escalate a complaint?

Does travel insurance cover hotel cancellations for illness?

What consumer protection laws apply to hotel cancellation disputes?

Can you dispute a hotel charge with your credit card company?