A proposal to cap credit card interest rates at 10 percent has the airline industry—and some frequent travelers—on high alert.

It’s a move that could provide relief to millions of Americans who are drowning in debt, but it might also be the end of the frequent flier points you’ve spent years collecting.

The debate intensified earlier this month when the president called for a one-year cap on credit card interest rates at 10 percent. He called the current rates of 20 to 30 percent “usury.”

The airline industry reacted with immediate concern. Industry advisers at the airline economics conference in Dublin this week warned that a cap would eviscerate the highly profitable loyalty programs that carriers depend on for survival.

How credit cards fuel your loyalty program

For decades, we’ve lived in a world where credit cards are the primary engine for travel rewards. But that engine runs on the high interest rates paid by other consumers. If that revenue disappears, banks may no longer find it profitable to buy billions of dollars in miles from the airlines.

The 10 percent solution

The proposed legislation, S.381 – 10 Percent Credit Card Interest Rate Cap Act, aims to amend the Truth in Lending Act to ensure interest rates don’t exceed 10 percent, inclusive of all finance charges.

Here are the facts:

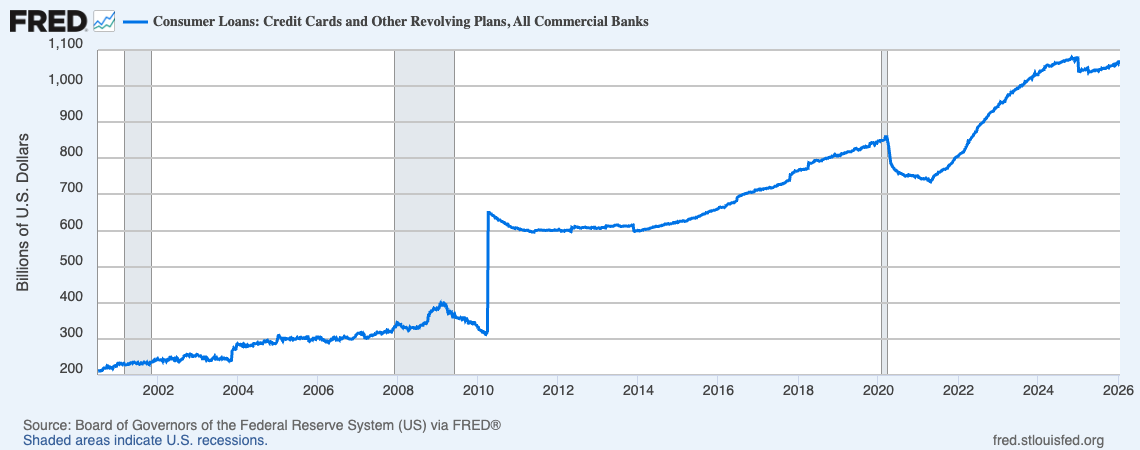

- Americans currently owe a record $1.23 trillion in credit card debt, according to the Federal Reserve Bank of New York.

- Average APRs for accounts that accrue interest sat at 22.3 percent in late 2025.

- Airlines like Delta generate billions annually by selling miles to banks—Delta alone received $8.2 billion from American Express in 2025.

The president’s proposal would cap credit card interest at 10 percent for a year, but critics say even that could permanently damage the loyalty ecosystem.

Who supports a 10 percent cap?

Supporters of this proposal include the president and a bipartisan group of senators like Bernie Sanders and Josh Hawley, who argue the move provides relief for working families. (Related: Why it’s time to let Spirit Airlines go.)

Among the opponents are the American Bankers Association and major card issuers, who warn the move will restrict credit access. Of course, the usual loyalty program fan blogs also believe this idea is worthless.

The question is irrelevant to me because I do not have an airline-specific credit card. The temporary cap of 10% will help those that carry a balance and may help them pay off their cards.

If the cap becomes permanent, it will probably make it harder for those with average to below average credit ratings to get a credit card–this may also include those just starting out in life.

Read more insightful reader feedback. See all comments.

So what do you think?

That brings us to this week’s question.

And a few follow-up questions:

- If you answered yes, do you think the loss of rewards is a fair trade for lower interest rates for everyone?

- If you answered no, do you believe banks will find another way to fund these “free” miles?

What do you think? Should the government be allowed to cap these rates even if it means the end of travel loyalty programs? Is it time to cap the rates and ground the points, or is the current system working for you?

My take

I’ve always been a loyalty program skeptic. But maybe it’s time we stop pretending these points are a gift and recognize them as a product of consumer distress. Americans are drowning in debt while chasing “free” flights. Consumers are paying for these points through sky-high interest rates that can trap them in endless cycles of debt.

Your turn

Are you concerned about the latest move to cap credit card interest rates? Or do you think this will be good for consumers? Our comments are open.

What you’re saying

Readers engaged in a complex debate over fairness versus economics. While some argued that high interest rates are predatory, others warned that capping them would destroy the rewards ecosystem and restrict credit access for those who need it most.

The subsidy problem

Linda Leeson and Mike called it what it is: the poor subsidizing the rich. They noted that high interest rates paid by those in debt fund the “free” travel of those who pay in full. Jennifer agreed, pointing out that banks only buy billions in miles because they make a killing on interest.

Unintended consequences

Donna S, a retired banker, warned that a 10% cap would make rewards programs unsustainable and restrict credit access to only the highest scores. Tim and George Schulman echoed this, predicting that banks would tighten underwriting standards, hurting the very people the law aims to help.

Personal responsibility vs. Usury

Jeff Long and Retiredfed Wisconsin argued against penalizing responsible savers who play the game correctly just because others can’t manage their finances. However, Tygar supported the cap, hoping Congress finally bans what they view as legalized usury.